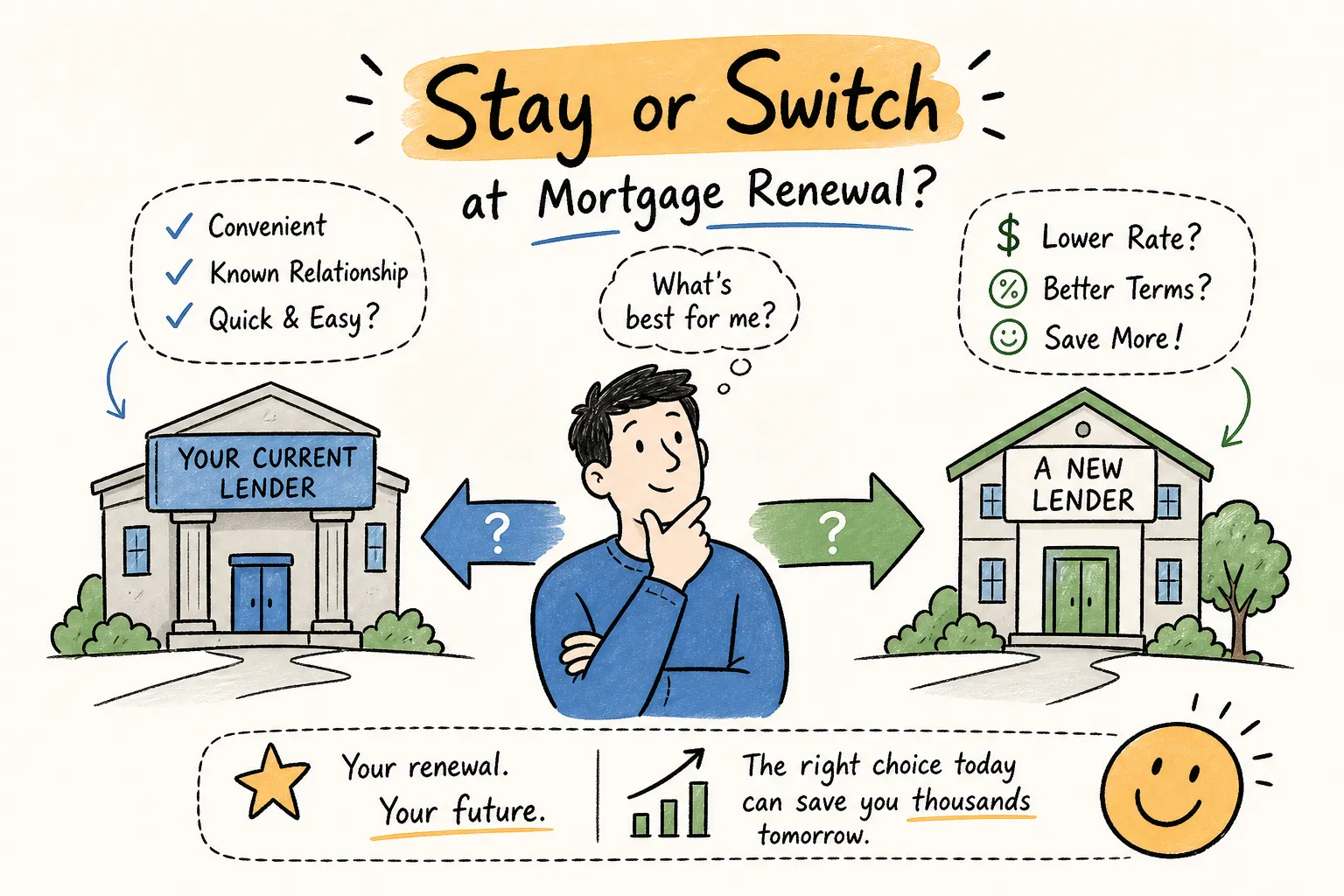

Should I switch lenders when my mortgage renews in Canada? It’s a question worth asking before you sign anything, because many Canadian homeowners get their renewal letter, glance at the rate, and sign it within a week. No shopping. No comparison. No negotiation. Just a signature and back to life. And that passivity is often exactly what lenders are counting on when they send that letter.

The gap between your lender’s renewal offer and what a competing lender would give you is rarely zero. In 2026, major banks are posting discounted renewal rates between 4.4% and 4.9%, while broker-sourced rates are sitting closer to 4.0%. That spread adds up fast on a $500,000 mortgage. According to Ratehub, the average borrower who shops at renewal instead of signing with their bank saves $13,857 over the term. That is not a rounding error.

This article gives you a clear framework: when switching lenders is worth it, what it actually costs, and how to compare your options without guessing. By the time you finish reading, you will know exactly what to do when that renewal letter lands.

Why most Canadians leave money on the table at renewal

Lenders send renewal offers banking on inertia. The rate in that letter is not their best offer. It is a starting point designed for borrowers who will not push back. Banks know that many clients will renew automatically to avoid the hassle of switching, so there is little incentive to lead with a competitive rate.

What makes this worse is that most borrowers have a 120-day window before their renewal date to lock in a new rate, penalty-free, though the exact timeline can vary by lender and mortgage contract, so check yours directly. That window is leverage. Use it early and you have time to shop, compare, negotiate, and move if necessary. Wait until the last two weeks before your renewal date and that leverage is gone. You are now making a rushed decision with no room to walk away.

The math alone justifies starting the process four months out. Even if you end up staying with your current lender after negotiating, you will almost certainly get a better rate than what the first letter offered.

The real savings: what switching lenders can put back in your pocket

A 0.25% rate improvement on a $500,000 mortgage saves roughly $91 per month and over $1,000 per year. Over a five-year term, that is more than $5,000. The Ratehub benchmark of $13,857 in average savings represents the upper range of what is possible when the rate gap is meaningful, but even a modest improvement compounds into real money over 60 months.

That said, not every rate difference justifies a switch. If the gap between your current offer and the competing rate is small, and switching costs are high, the net savings can disappear or barely break even. A $25 per month improvement saves roughly $1,500 over five years. Legal and discharge fees alone can run $500 to $2,500 or more in Ontario depending on complexity. At that margin, you may be better off negotiating with your current lender than going through a full lender transfer.

The key variable is always the spread between what you are offered and what else is available, measured against the total cost of making the move. Run the actual numbers before you decide anything.

What switching lenders actually costs: the fees and timeline

Switching at renewal, rather than mid-term, means you avoid prepayment penalties entirely. That is one of the most important timing points in this whole conversation. A mid-term break can cost thousands of dollars in penalties. At renewal, that risk is off the table.

The fees you will typically pay to move your mortgage at renewal break down into four categories:

- Discharge fee from your current lender: $0 to $400

- Assignment or transfer fee: $5 to $500 depending on the lender

- Appraisal if the new lender requires one: $150 to $500

- Legal or title registration fees: $500 to $2,500 depending on complexity and province

In Ontario specifically, discharging and re-registering a charge on title requires a lawyer, and those two steps drive most of the legal cost. Some lenders will cover part or all of these fees as an incentive to win your mortgage, cash bonuses up to $4,000 are available in the current market, so it is worth asking directly what the new lender will cover before you assume you are paying out of pocket.

The process itself takes 45 to 90 days from application to completion. You receive your renewal offer, start shopping, submit an application to the new lender, complete their underwriting review, and then a lawyer handles the registration and transfer. That is not a two-day process. Starting late creates unnecessary pressure and reduces your ability to walk away if something does not look right.

What the new lender will ask you to provide

When you switch lenders, you go through a re-approval process. The new lender will typically want your current renewal statement, proof of income (recent pay stubs or tax documents), government-issued photo ID, property tax documents, home insurance confirmation, and possibly a new appraisal. Unlike renewing with the same lender, you do not get to skip underwriting. Requirements can vary by lender and mortgage type, so confirm the document list early.

One important distinction many homeowners do not know: under OSFI’s current rules, borrowers switching lenders at renewal on an uninsured mortgage are not required to pass the mortgage stress test the same way new purchase applicants are. As long as the loan amount and amortization stay the same, OSFI does not expect lenders to apply the minimum qualifying rate to these straight switches. That change, confirmed in November 2024, removes a significant barrier that previously made switching harder than staying. Your new lender will still review your credit and income, but the formal stress test hurdle does not apply in the same way.

Should I switch lenders when my mortgage renews? The decision factors

As a general rule of thumb, a rate improvement of 0.30% or more on a mid-to-large mortgage balance often clears the break-even point after switching costs, but always run your own calculation with actual fee estimates before acting on that number. For smaller balances or tighter rate gaps, negotiating with your current lender may produce a better net outcome. The math is straightforward: total interest saved at the new rate over the term, minus the all-in cost of switching. If that number is positive and meaningful, switching is worth pursuing.

Your financial profile matters too. If your income has become irregular, your credit score has shifted, or you have taken on new debt since your last renewal, a new lender may not approve you at the advertised rate. In that case, staying with your current lender is sometimes the smarter path. Existing lenders often have more tolerance for file complexity at renewal than a new lender seeing your application cold.

One distinction worth making clearly: switching lenders at renewal is not the same as refinancing. A straight switch transfers your existing mortgage balance to a new lender at the same amortization, refinancing changes the mortgage amount, restructures the term, or accesses equity. If your goal is to pull out home equity for renovations or consolidate debt at renewal, you are in refinancing territory, which involves different costs, different qualifying criteria, and a different conversation entirely.

How to compare mortgage rates at renewal: what to look beyond the rate

Rate is the starting point, not the whole picture. When you compare offers from multiple lenders, look at prepayment privileges (the percentage of your mortgage balance you can pay down annually without penalty), penalty calculation methods, and portability rules. A lower rate with a punishing penalty clause can cost you more than a slightly higher rate with borrower-friendly terms if you sell or need to break the mortgage before the term ends.

Porting a mortgage in Canada is particularly relevant in Ontario. If you move during your term, a portable mortgage lets you transfer your rate to the new property. Not all lenders offer the same portability terms, and the Ontario land registration process means that transferring a mortgage between properties involves its own legal and administrative steps. A rate that looks great on paper can become expensive if the product restricts your flexibility during the term.

- Prepayment privileges: How much can you pay down annually without penalty? 10%, 15%, 20%?

- Penalty calculation method: A fixed three-month interest penalty versus an interest rate differential (IRD) penalty can mean the difference between roughly $2,000 and $15,000 or more, depending on your outstanding balance and the rate gap, always ask how your potential new lender calculates penalties before you sign.

- Portability terms: Can you take the mortgage to a new property if you move, and under what conditions?

How a mortgage broker shops the market so you don’t have to

Going lender to lender on your own means filling out multiple applications, triggering multiple credit inquiries, and comparing offer documents written in each lender’s specific language. Most homeowners do this once, maybe twice, then stop because it gets confusing and time-consuming. That typically means settling for the second or third option rather than the best available one.

At Done Mortgage, Swatti Malik and the team shop rates across a network of lenders in a single step. Competing offers get pulled, compared, and evaluated for both rate and fine print before you sign anything. The team identifies which lenders will match or beat your current rate, flags penalty clauses and portability terms that matter for your situation, and negotiates on your behalf. The process involves less paperwork duplication on your end and can surface options that a direct bank search may not reach.

Renewal happens every few years but the dollar impact lasts the entire term. It deserves more than a five-minute glance at a letter your bank sent hoping you would not read carefully. For most Canadian homeowners asking whether switching lenders makes sense at renewal, the real question is whether you want to spend several weeks doing the comparison yourself or have someone who does this every day do it for you.

Should I switch lenders when my mortgage renews in Canada? A quick checklist

- Request competing rate quotes at least 90 to 120 days before your renewal date (confirm your exact window with your lender)

- Calculate your total switching costs: discharge fee, transfer fee, appraisal, and legal fees

- Compare total interest paid at each rate over the full term, not just the monthly payment

- Check prepayment privileges, penalty calculation method, and portability terms on every offer

- Assess your financial profile: income stability, credit, and any new debt since last renewal

- Confirm whether a straight switch meets your goals, or whether you actually need to refinance

- Ask each new lender what switching costs, if any, they will cover

The bottom line on switching lenders at renewal

The honest answer to whether you should switch lenders when your mortgage renews in Canada is: it depends on the math. If the rate difference clears the cost of switching and your financial profile supports a clean re-approval, switching is almost always worth exploring. If the gap is narrow or your situation has changed, negotiating with your current lender may be the smarter play.

What is never the right move is signing the renewal offer without looking at what else is available. Your lender’s first letter is not their best number. It rarely is.

Start early, ideally 90 to 120 days before your renewal date. Know your numbers. Understand what switching actually costs in your situation. And if you want Done Mortgage to compare rates and answer “should I switch lenders when my mortgage renews in Canada?” on your behalf, reach out before your renewal window closes.