Table of Contents

Mortgage Broker Oakville services are becoming increasingly important as homeowners look beyond interest rates and focus on long-term mortgage planning, refinancing flexibility, home equity strategies, and overall financial outcomes.

Buying a home or refinancing in Oakville isn’t usually just about getting approved for a mortgage.

For many homeowners, the bigger question is whether they’re making the right long-term financial decision.

Oakville has become one of the most established housing markets in the GTA. Many homeowners have built substantial equity over the years, property values remain among the highest in the region, and mortgage balances tend to be larger than average. As a result, small mortgage decisions can have a significant financial impact.

That’s why many Oakville borrowers look beyond interest rates alone.

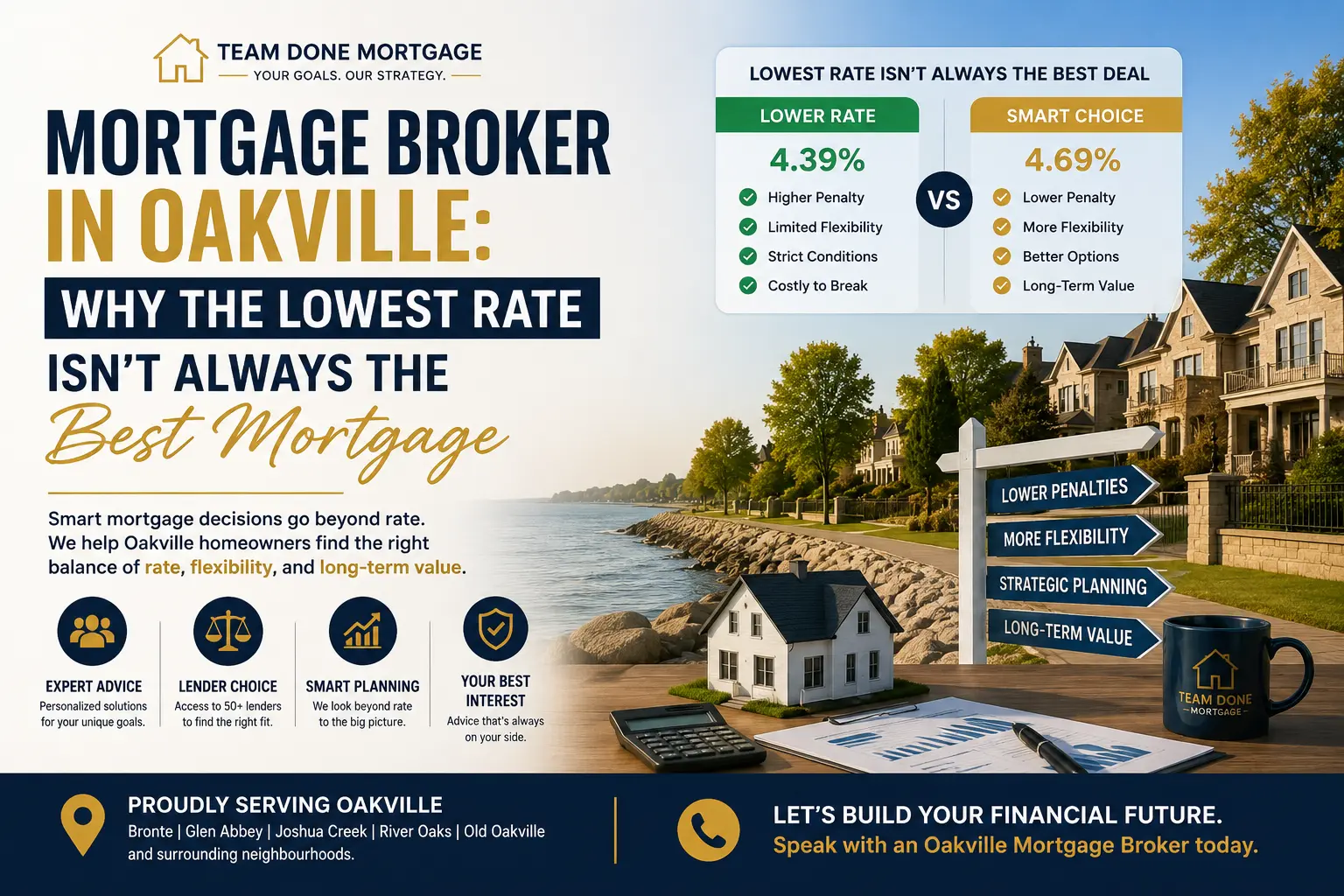

At Done Mortgage, we often speak with homeowners who are focused on finding the lowest available rate. While rate matters, it’s only one part of the picture. Mortgage penalties, refinancing flexibility, renewal options, and future plans can often have a bigger impact on your finances than a slight difference in rate.

Why Oakville Borrowers Approach Mortgages Differently

Many Oakville homeowners are not first-time buyers.

They are often:

- Established professionals

- Corporate executives

- Business owners

- Growing families

- Long-time homeowners with significant equity

Unlike buyers primarily concerned about qualifying, these borrowers are usually asking more strategic questions:

- Should I refinance now or wait?

- Is it worth breaking my mortgage?

- How can I use my home equity effectively?

- Should I stay with my current lender at renewal?

- Is a lower rate worth paying a large penalty?

The answers depend on much more than today’s advertised mortgage rate.

Who We Help in Oakville

Professionals

Oakville is home to many professionals working in finance, healthcare, technology, engineering, and professional services.

These borrowers often have strong income profiles but may also have bonuses, stock compensation, or variable income that requires proper lender selection.

Executives

Executive compensation can be more complex than traditional employment income.

Bonus structures, dividends, stock options, and partnership income often require additional documentation and careful positioning during the mortgage approval process.

Move-Up Buyers

Many Oakville families are upgrading within the community.

Whether moving from a townhome to a detached property or upgrading into neighbourhoods like Glen Abbey, Joshua Creek, Bronte, or Old Oakville, mortgage planning becomes increasingly important as property values rise.

Equity-Rich Homeowners

A large number of Oakville homeowners have accumulated substantial equity simply through years of ownership and market appreciation.

The challenge is determining how to use that equity wisely without creating unnecessary borrowing costs or financial risk.

Common Mortgage Mistakes Oakville Homeowners Make

Focusing Only on Interest Rates

One of the biggest misconceptions in the mortgage market is that the lowest rate automatically means the best mortgage.

It doesn’t.

A mortgage with a slightly lower rate but restrictive terms can become far more expensive if you need to refinance, move, or break the mortgage before maturity.

Ignoring Mortgage Penalties

Many borrowers don’t review penalty calculations until they decide to refinance or sell.

By then, the costs can come as a surprise.

This is especially important for larger mortgage balances, where penalties can easily reach thousands of dollars.

Thinking Only About the Current Term

Mortgage decisions should support long-term financial goals.

Many homeowners focus exclusively on the next five years and ignore:

- Future refinancing needs

- Investment plans

- Family growth

- Retirement goals

- Potential moves

A mortgage should support future flexibility, not limit it.

Breaking a Mortgage Without Analysis

When rates decline, many homeowners immediately consider switching lenders.

However, lower rates do not always mean savings.

Before breaking a mortgage, it’s important to compare:

- Penalty costs

- Remaining term

- Interest savings

- Future plans

A detailed review often reveals a very different financial picture than expected.

Not Using Home Equity Strategically

Home equity can be a powerful financial tool.

Many homeowners use equity for:

- Renovations

- Investment properties

- Debt consolidation

- Business opportunities

- Education expenses

However, accessing equity without a clear plan can create unnecessary costs.

How Our Mortgage Approach Is Different

We Look Beyond the Rate

Rates matter.

But we also review:

- Penalty structures

- Flexibility

- Refinancing options

- Renewal opportunities

- Long-term costs

The goal is to find a mortgage that fits your financial objectives—not just today’s market.

Exit Strategy Planning

Every mortgage should include an exit strategy.

Before selecting a lender, we discuss:

- Potential moves

- Refinancing plans

- Future borrowing needs

- Investment goals

Understanding how you’ll eventually leave a mortgage is just as important as understanding how you’ll enter it.

Comparing More Than One Lender

Different lenders offer different advantages.

Some provide:

- Better flexibility

- Lower penalties

- Easier refinancing

- Stronger renewal options

The right lender isn’t always the one with the lowest advertised rate.

Planning Beyond the Current Mortgage Term

A mortgage is rarely a one-time decision.

Most homeowners will refinance, renew, upgrade, or restructure their mortgage at some point.

Planning ahead can help avoid expensive surprises later.

Mortgage Services Available in Oakville

Home Purchases

Whether you’re buying your first Oakville property or upgrading to a larger home, lender selection and mortgage structure play an important role in long-term affordability.

Mortgage Refinancing

Refinancing may help homeowners:

- Access equity

- Consolidate debt

- Improve cash flow

- Fund renovations

- Support investment opportunities

Timing and penalties should always be reviewed before proceeding.

Mortgage Renewals

Many homeowners automatically accept their lender’s renewal offer without comparing alternatives.

Renewal is often the best time to reassess:

- Rates

- Mortgage structure

- Future plans

- Equity opportunities

Oakville Mortgage FAQs

Fixed or Variable Mortgage: Which Is Better for Higher-Income Borrowers?

There is no universal answer.

The right choice depends on your risk tolerance, cash flow needs, financial goals, and comfort with changing interest rates.

When Should I Refinance My Mortgage?

Refinancing may make sense when you can improve your financial position, access equity strategically, or reduce higher-interest debt.

A penalty review should always be part of the decision.

Is Working With a Mortgage Broker Better Than Going Directly to a Bank?

A bank can only offer its own products.

A mortgage broker can compare multiple lenders and mortgage structures to help find a solution that fits your situation.

Should I Break My Mortgage If Rates Drop?

Not necessarily.

The answer depends on the penalty, remaining term, interest savings, and your future plans.

Can I Use Home Equity to Invest or Upgrade?

Potentially, yes.

Many Oakville homeowners use home equity to fund renovations, investment properties, or other financial goals. The key is ensuring the strategy makes sense within your broader financial plan.

Get Mortgage Advice From an Oakville Mortgage Broker

Oakville homeowners often have strong financial profiles, but larger mortgage balances and significant home equity create more complex decisions.

At Done Mortgage, we help borrowers look beyond rates and evaluate the full picture—mortgage structure, flexibility, penalties, refinancing opportunities, and long-term financial goals.

Whether you’re buying, refinancing, renewing, or exploring ways to use your home equity more effectively, getting advice early can help you avoid costly mistakes later.

If you’re planning your next mortgage move in Oakville, speaking with a mortgage broker can help you make a more informed decision.