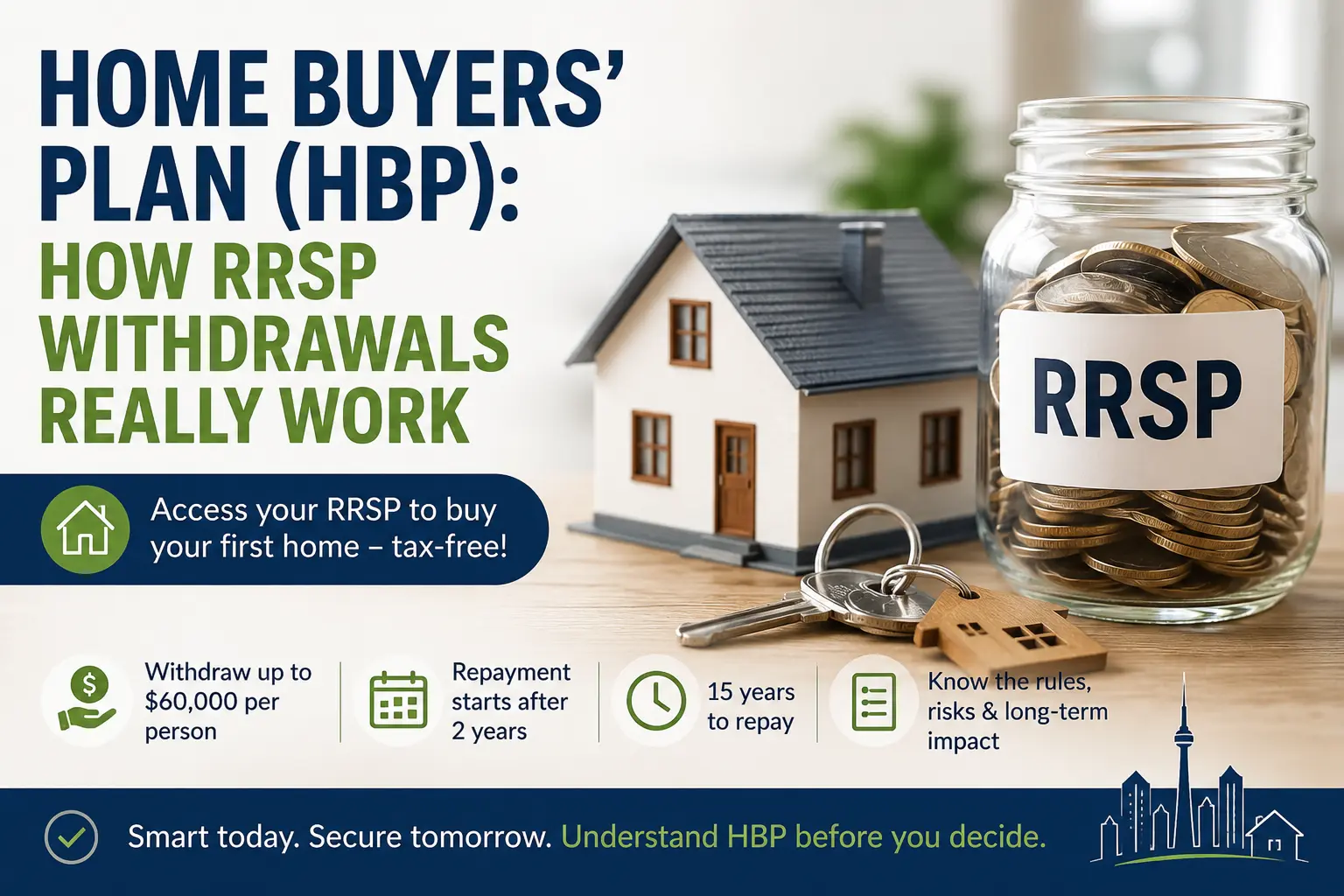

Home Buyers Plan Canada allows eligible first-time home buyers to withdraw up to $60,000 from their RRSP to help fund a home purchase. While this can improve affordability, many buyers overlook the long-term impact on retirement savings and future wealth creation.

Table of Contents

What the Home Buyers’ Plan (HBP) Actually Is

The Home Buyers’ Plan (HBP) lets you pull money from your RRSP to buy a home.

- You can withdraw up to $60,000 per person

- Couple = $120,000 total

Sounds great? Yes.

But here’s the reality:

👉 It’s not free money

👉 It’s a loan from your future retirement

How Much You Can Withdraw

- Individual: $60,000

- Couple: $120,000

Conditions:

- Must be a first-time home buyer (or meet CRA exceptions)

- Funds must be in RRSP for at least 90 days

Repayment Timeline (With Example)

You don’t repay immediately.

- Repayment starts after 2 years

- Total repayment period: 15 years

Example:

- You withdraw: $60,000

- Annual repayment: $4,000/year

If you skip:

That year’s amount gets added to your taxable income

What Happens If You Miss Repayments

Let’s not sugarcoat this.

If you don’t repay:

- CRA treats it as income

- You pay tax on that portion

Example:

- Miss $4,000 repayment

- That $4,000 is added to your income

- You pay tax based on your bracket

It’s basically a forced tax penalty

How HBP Impacts Your Retirement (Most Ignored Part)

This is where people mess up badly.

You’re pulling money out of a tax-deferred growth engine.

Let’s say:

- You withdraw: $60,000

- Average return: 6%

After 15 years, that money could have been:

👉 ~$143,000

Instead:

- You’re slowly putting it back

- Missing compounding growth

Real cost = lost investment growth, not just the withdrawal

Common Mistakes First-Time Buyers Make

1. Using HBP Without a Repayment Plan

They assume “I’ll handle it later”

Reality:

Most don’t → leads to tax hits

2. Emptying Their RRSP Completely

Now they have:

- No retirement cushion

- No emergency buffer

3. Using It When They Don’t Need It

If you already have enough down payment:

You’re just hurting future wealth

4. Ignoring Opportunity Cost

They see:

“$60K for house”

They don’t see:

“$80K–$100K+ lost future value”

Does Using HBP Make Your Mortgage Stronger or Weaker?

This is where you need clarity.

Stronger:

✔ Increases your down payment

✔ Helps you qualify easier

✔ Can reduce CMHC insurance cost

Weaker:

Reduces your financial reserves

Shows less post-closing liquidity

Adds future repayment pressure

Lenders don’t care about HBP itself

They care about your overall financial stability

Smarter Alternatives (Most People Ignore These)

If you’re thinking long-term, look at:

1. First Home Savings Account (FHSA)

- Tax-free contributions

- Tax-free withdrawals

Way better than HBP if planned early

2. Keep RRSP Invested + Use Smaller Down Payment

- Pay slightly higher mortgage

- Keep compounding working

3. Combine HBP + Cash Strategy

- Don’t max it out blindly

- Use only what’s needed

FAQ

Is HBP free money?

No.

It’s your own money — with a repayment obligation.

Do I pay interest on HBP?

No interest.

But the real cost is lost investment growth.

Can I repay faster?

Yes.

No penalty for early repayment.

Links

- CRA Home Buyers Plan Rules

- CMHC First-Time Home Buyer Resources

- First-Time Home Buyer Mortgage

- FHSA Guide RRSP vs TFSA

- Mortgage Broker Toronto