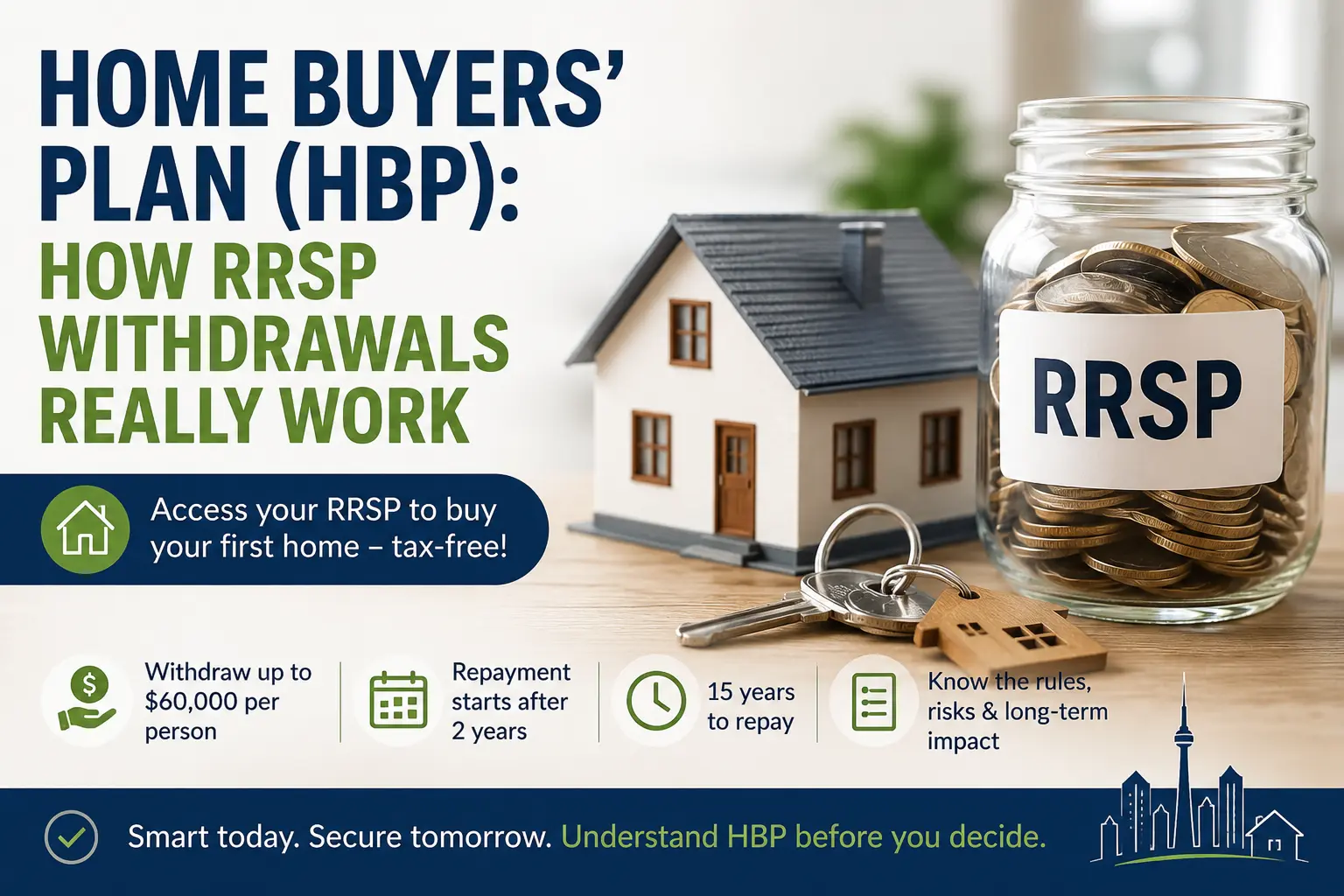

First Time Home Buyer Incentive is a government shared-equity program designed to help eligible Canadians reduce their mortgage payments. While it can improve affordability, many buyers underestimate the long-term cost of giving up a portion of their future home appreciation.

Table of Contents

First-Time Home Buyer Incentive in Canada:

What the First-Time Home Buyer Incentive Actually Is

The First-Time Home Buyer Incentive (FTHBI) is not free money.

It’s a shared equity deal with the government.

- Government gives you:

- 5% for resale homes

- 5% or 10% for new builds

In return:

- They own that % of your home’s value

- When you sell → you pay back that same % of the new value, not what you borrowed

This is where most people get fooled.

How Much the Government Really Gives (Example)

Let’s say:

- Purchase Price: $600,000

- You take 5% incentive = $30,000

Sounds helpful? Yes.

But here’s the real math:

- Your mortgage reduces → slightly lower monthly payment

- BUT you’ve just given away 5% ownership of your property

Real Example: What You Repay After 5 Years

Let’s not pretend. Prices don’t stay flat.

Scenario:

- Buy at: $600,000

- Incentive: $30,000 (5%)

- After 5 years: property grows to $750,000

Now repayment:

- You owe 5% of $750,000 = $37,500

You borrowed $30K → you repay $37.5K

That’s not cheap money. That’s equity dilution.

How Repayment Actually Works

You repay when:

- You sell the property

- You refinance

- Or after 25 years (max term)

Important:

- You can repay early anytime

- The amount is always tied to market value, not original loan

Hidden Downsides Nobody Explains

Let’s cut the bullshit. Here’s what brokers don’t highlight clearly:

1. You’re Giving Away Future Gains

If your property grows → government benefits with you

2. It Can Complicate Refinancing

Lenders don’t love shared equity structures

- More paperwork

- Extra approvals

- Slower deals

3. Limits Your Buying Power

There are income + price caps

Meaning:

- You’re restricted in what you can buy

- Not ideal in expensive markets like Ontario

4. Psychological Trap

People think:

“I’m getting help”

Reality:

You’re trading long-term wealth for short-term affordability

How This Affects Your Equity & Future Refinancing

This is where smart buyers think differently.

Without FTHBI:

- You own 100% of appreciation

With FTHBI:

- You share gains → lower net equity

That affects:

- Refinancing options

- Access to HELOC

- Investment leverage later

👉 If your plan is to upgrade, invest, or refinance, this matters a lot.

When It Actually Makes Sense

This is not useless. It works in specific situations:

✔ You’re cash-constrained

✔ You need lower monthly payments to qualify

✔ You plan to sell short-term (less appreciation impact)

✔ You’re buying in a slow-growth market

When It Doesn’t Make Sense

Be honest with yourself:

You expect strong price growth (Ontario/GTA)

You want to build equity fast

You plan to refinance or invest later

You can already afford without it

In these cases, you’re giving away upside for no real reason.

FAQ

Does it reduce my mortgage?

Yes — slightly.

But not enough to justify giving up equity in many cases.

Does it affect resale?

Yes.

- You must repay based on market value

- Cuts into your profit

Is it free money?

No.

It’s a shared investment, not a grant.

Can I buy it out early?

Yes.

But you repay based on current market value, not original amount.

When You Should Speak to a Mortgage Expert

Don’t guess here. This is where people screw up.

You should get advice if:

- You’re close to affordability limits

- You’re deciding between higher down payment vs incentive

- You want to understand long-term impact on wealth

A proper mortgage strategy can save you way more than this incentive.

Final Verdict (No Sugarcoating)

FTHBI is:

- Helpful for entry

- But expensive long-term in rising markets

If you’re buying in Ontario and expect appreciation…

You’re probably better off keeping full ownership.

Links

- CMHC First-Time Home Buyer Incentive Information

- Government of Canada Home Buying Programs

- First-Time Home Buyer Mortgage

- FHSA Guide RRSP vs TFSA

- Mortgage Broker Toronto