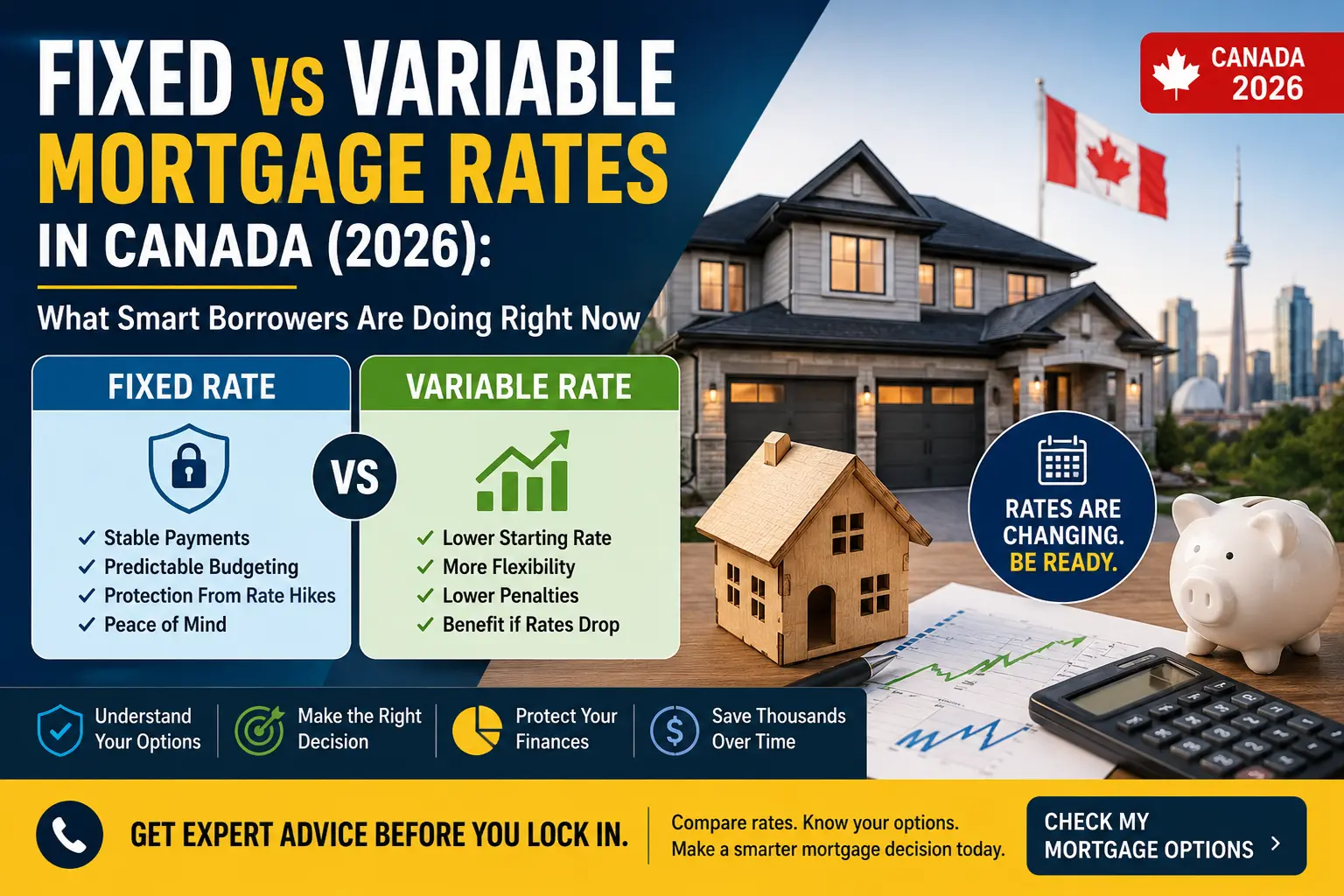

Why Banks Are Pushing Fixed Rates has become a common question among Canadian homeowners as bond yields rise and lenders increase fixed mortgage pricing despite the Bank of Canada holding rates steady.

I’ve spent the last week in my Brampton office speaking with homeowners who are feeling a very specific kind of whiplash. The Bank of Canada just announced they are holding the policy rate at 2.25%, yet people are walking into their banks and being quoted higher rates than last month.

Table of Contents

What’s going on?

The truth is, while the central bank is standing still, the bond market is moving fast. Government of Canada bond yields have recently ticked up to 2.7% due to geopolitical energy shifts. This has created a massive disconnect: Variable rates are stable, but fixed rates are suddenly getting expensive. If your bank is currently “strongly suggesting” you lock into a 5-year fixed rate, you need to ask yourself whose interests they are protecting.

1. Decoding the “Fixed Rate Trap”

It is a common mistake to think the Bank of Canada controls every rate you see. They don’t.

- The Variable Side: These rates move only when the BoC moves its prime rate (currently 2.25%).

- The Fixed Side: These are essentially a prediction of the future, influenced by those 2.7% bond yields. If you are looking for ways to avoid this trap and protect your renewal, read our 2026 GTA Mortgage Survival Guide.

Because bond yields are volatile right now, banks are nervous. When they push a fixed rate, they are asking you to pay a premium for “security.” But in 2026, where we expect rates to eventually stabilize around 3.25% by 2030, locking in at a peak today could cost you thousands in the long run.

2. Why the Bank’s “Security” is a Sales Tactic

Whenever the news cycle gets loud with talk of inflation or energy shifts, banks use that fear to sell fixed-rate contracts.

But look at the actual 2026 data. Home affordability actually improved in 12 of 13 major Canadian cities in January. In Toronto, the average price dropped by $7,100. The market isn’t spiraling—it’s adjusting. Choosing a variable rate isn’t “gambling”; it’s a strategic bet that you can handle short-term noise to win on long-term flexibility.

3. The “Done Mortgage” Advantage for Self-Employed GTA Pros

If you are self-employed in Ontario, the rate is only half the battle. Most banks look at your tax returns and see “risk.” We look at your business and see “equity.”

We specialize in repositioning files using corporate add-backs and retained earnings before we ever hit “submit” to a lender. Whether we choose a variable stability path or a shorter-term fixed, our goal is to ensure your file is structured for approval—not just another “declined” notice from a bank that doesn’t understand your positioning.

March 2026: Frequently Asked Questions

Wait, why did my bank quote me a higher fixed rate if the BoC held at 2.25%?

Your bank is watching the bond market, not just the BoC. With bond yields rising to 2.7%, fixed rates are being repriced upward regardless of what the central bank does.

What is the current “Stress Test” I need to pass?

As of January, the average 5-year fixed rate was 4.40%, meaning you must prove you can afford a mortgage at roughly 6.40%.

Is 2026 actually a good time to buy in Brampton or Toronto?

Yes, but for a different reason than you think. Inventory has rebuilt to 4.9 months of supply. It’s a buyers’ market, meaning you have the leverage to negotiate price, even if rates aren’t “crashing” yet.

I’m self-employed—will a variable rate hurt my approval?

Not if the file is structured correctly. By using deposit analysis and corporate income add-backs, we can often show a much stronger financial position than a standard T4 employee.

Links

- CRA Home Buyers Plan Rules

- CMHC First-Time Home Buyer Resources

- First-Time Home Buyer Mortgage

- FHSA Guide RRSP vs TFSA

- Mortgage Broker Toronto